Short Study on SMS

Front picture – the Rossing open pit mine In Namibia 7kms away from SMS’s new tenement acquisition. The most productive uranium mine in the world.

Disclaimer: This report is not JORC compliant. We use forward-looking statements. All valuations indicated are our own in-house best estimates. This is not financial advice. It is a document for our club members information and research purposes. It outlines why we have added SMS into our Ten Bagger Portfolio.

Note: Our ten-bagger portfolio takes swing-for-the-fences type bets on stocks we believe have the ability to 10-bag over the coming 24-36 months, but as they are often risky, firstly we examine our downside if things go wrong.

Star Minerals (ASX code SMS): Potential downside

SMS has around A$ 400k in cash and a tight share register with only 94.7 million shares on issue. At today’s share price of 4.5 cents, SMS’s tiny market cap of A$4.3 million frankly values it at little more than an empty ASX listed shell company.

The SMS share price has fallen 80% since it first IPO’ed at 20 cents in late 2021. So we are now getting a cheaper entry than most shareholders. But even during the recent weak market with little news SMS share price made floor between 3 to 3.5 cents, meaning our downside risk from here is around 30% in a bad case.

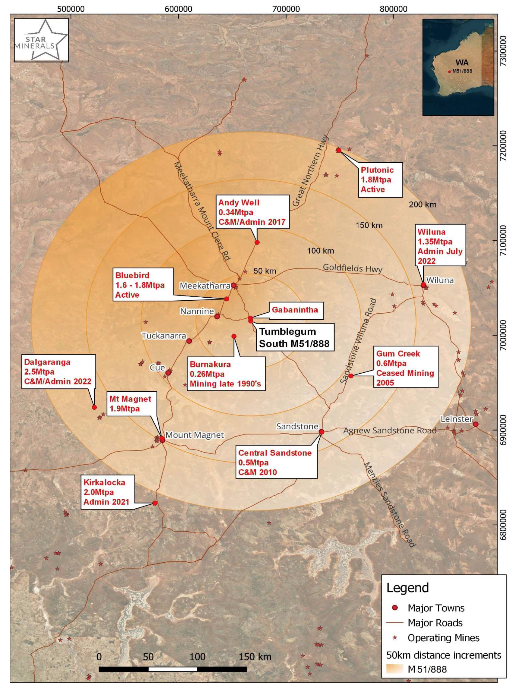

Tumblegum – Gold deposit, WA.

SMS owns Tumblegum, a 45,000 oz JORC’ed gold resource in West Australia. At today’s gold price of A$3,800 this resource has an in-ground value (IGV) of around A$170 million. Its normal to value a company at around 3-5% of its IGV. On that basis SMS should have a market around A$5-8 million. (5-8 cents per share). So, we believe their gold asset not only underpins SMS’s current market cvalue, reducing downside potential- but it also means any extra assets are free.

SMS have completed their scoping study(SS) local Flora and fauna and heritage surveys on the site – so it’s almost “shovel-ready”. Map 1 below shows how Tumblegum is surrounded by several operating gold mines. There are three gold processing plants within 150kms and SMS is currently in negotiation with them to obtain a schedule to process their ore so they can start mining it.

The SMS Scoping study estimates that SMS could to start to profitably open pit mine the Tumblegum Resource for a start up cost of between A$1.7 – A$3.9 million. However, this could be reduced by bringing in mining sub-contractors on a profit-share basis. The SS estimates that at today’s gold price, SMS should then be able to generate a profit between A$10-20 million from one 18-month mining campaign of the resource.

Therefore, with a relatively modest Cash raise it possible this gold asset could soon start generating enough cash for SMS to fulfill its new Cobra Uranium deal In Namibia without SMS necessarily undergoing excessive dilution.

Cobra – the potential upside.

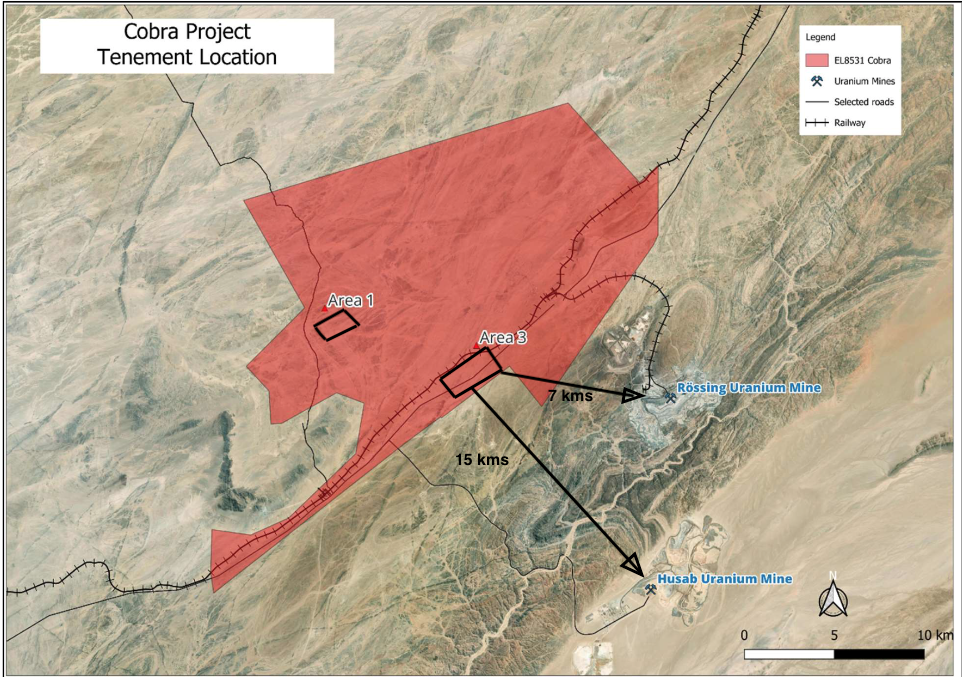

SMS has just entered into a deal to acquire up to an 80% stake in Cobra, a large Uranium prospective tenement in Namibia. next three year by spending USD 3.95 million developing the asset.

Cobra already contains an indicated JORC equivalent resource pf 9 million Lbs of U3O8. Under their acquisition deal SMS has the right to ultimately acquire up to 80% of this asset.

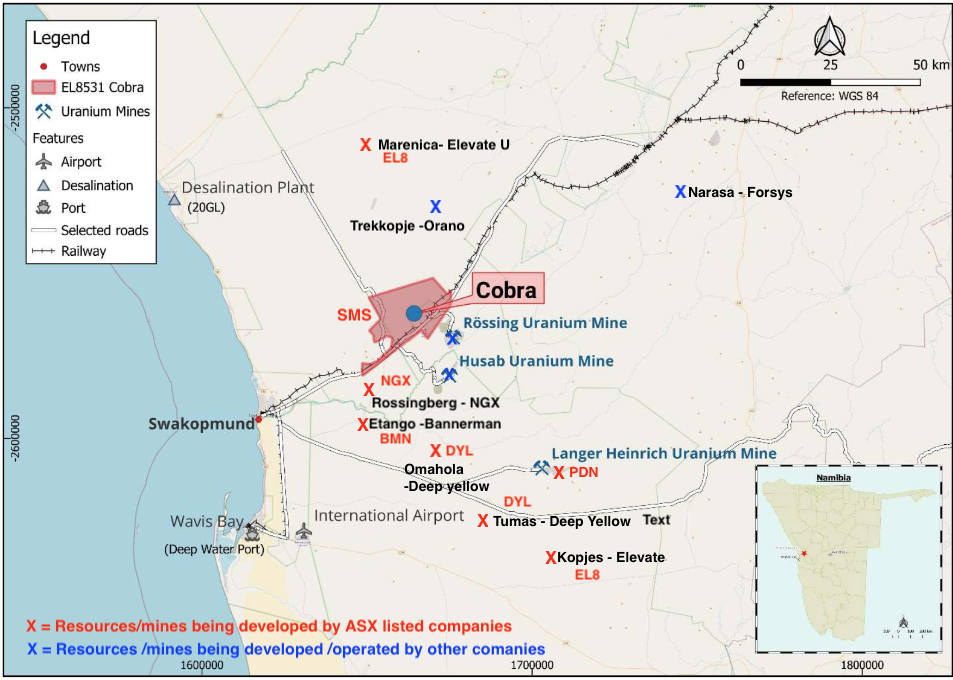

The map below shows the Cobra tenement sitting right in the heart of Erongo Province the centre of Namibia’s rich Uranium resources. Over the last two decades several huge U resources have been developed there three have become some of the world’s largest uranium mines that have now made Erongo province and Namibia the world’s third largest uranium producer.

Cobras three Giant Neighbours.

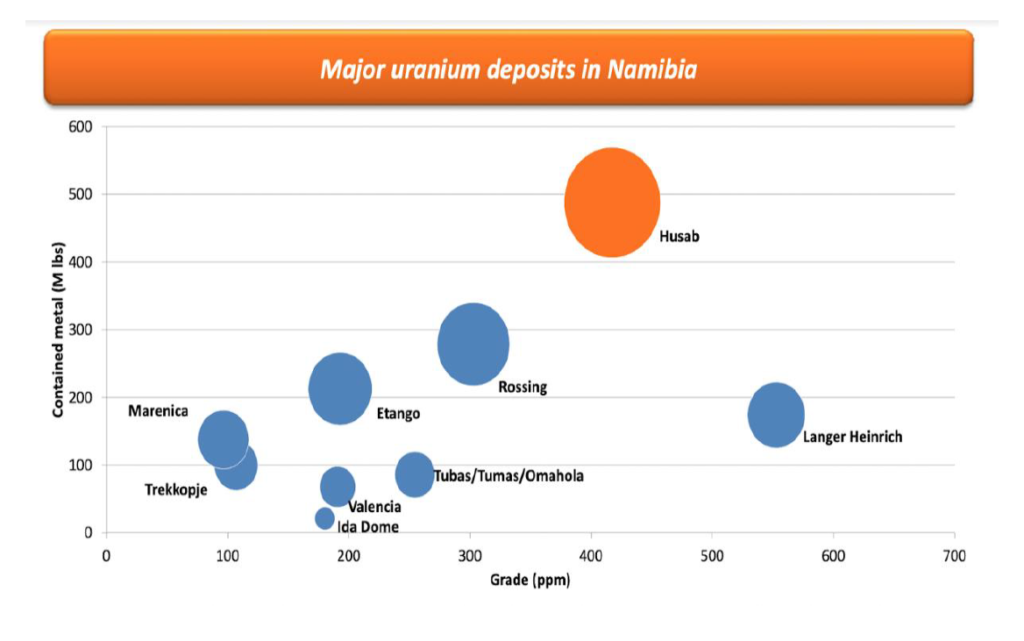

1. Rossing – Cobras Area 3 initial JORC resource discovery lies only 7kms away from the giant Rossing Uranium resource and mine (see cover pic) and it has similar geology. Rossing is one of the world’s largest open pit mines. It is owned by CNNC (China National Nuclear Corp), opened in 1978 and is the oldest operating uranium mine in the world. Last year it produced 5% of the worlds uranium supply and overall has produced more uranium than any other mine in the world. Yet this giant nearby resource is still estimated to hold well over 300 mill lbs of uranium.

2. Hussab – Lying around 15 Kms away to the south west is the Husab mine on another monster resource estimated to hold around 270 Mlbs of U3O8. The Hussab resource was only discovered in 2009 and the mine opened in 2013. It is now the second largest Uranium mine in the world after Cameco’s MacArther River Mine in Canada.

3. Langer Heinrich – Around 45ms south is a third giant resource: Langer Heinrich estimated to contain over 300 Mlbs of U308. Langer Heinrich is mined by ASX listed Paladin Resources.

These Mines caused two of the biggest ASX equity gains ever:

1. In the last uranium bull run from 2003 to 2007, Paladin Resources PDN – then just a small ASX Uranium explorer like SMS valued at a few cents, discovered and started developing Langer Heinrich. As the resource expanded, PDN’s stock price ran up from a low of A$0.01 cents to a high of A$120. A legendary 44,600% in three years. Today Paladin has a market cap of A$2.9 billion.

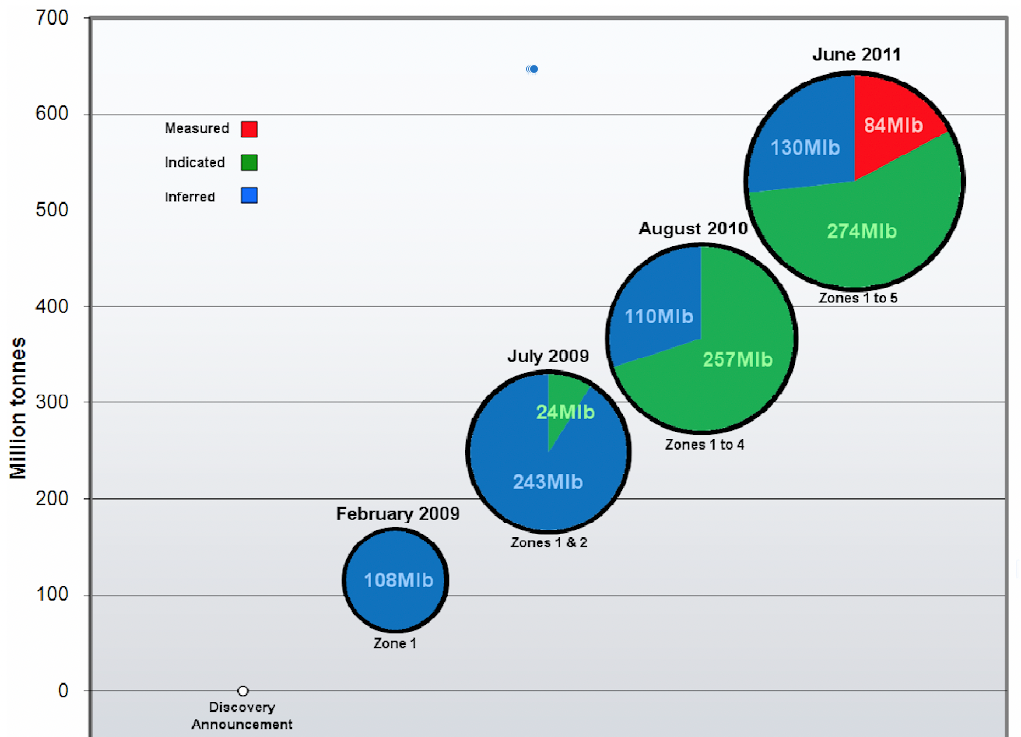

2. Husab – Around the same time, Extract Resources (XTR) another small ASX listed Uranium explorer – discovered and started developing the nearby Husab resource. As it kept enlarging with further drilling XTR shares ran up from 3 cents to a High of A$18. – a gain of around 20,000% in three years. XTR was later bought out in 2012 by China general Nuclear for $8.80 per share which valued the Husab resource at A$2.2 billion.

Could Cobra prove to be the next big resource in Erongo?

Chairman Ian Stuart has said “We sees enormous potential to upgrade and increase the existing estimates”. SMS also noted in their latest ASX announcement that “the whole tenement has prospective geology for significant resource expansion and further discoveries.”

Cobra is notable that given its huge 297 sq km size and its central location it the Erongo Uranium belt, it has not been drilled much. This is because it was held for a long time by a French family office. In 2015 they funded some limited drilling in two areas and almost every drill hole sunk indicated levels of Uranium.

Two main strike areas (Areas 1 and 3) were identified for follow-up drilling to obtain a foreign estimate JORC which indicates a resource of 9 Mlb’s U308. Both strike zones remain open on all sides. SMS will pay to extend drilling on them.

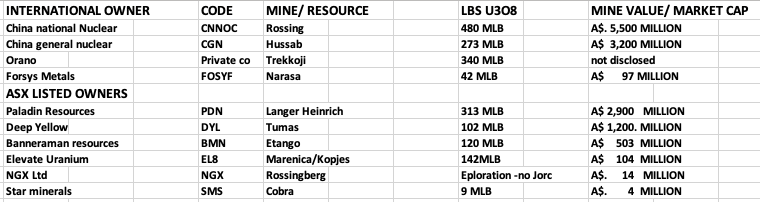

SMS appears undervalued compared to its ASX peers.

In addition to the three huge mines nearby, the map above shows Cobra is surrounded by other large uranium resources all around it Those surrounding resources with JORC’s are valued at between A$100 million to A$5 billion….and rising. Below is a list of the resources surrounding Cobra and their estimated:

As you can see Several of the surrounding resources are being developed by ASX listed companies whose share prices have appreciated strongly in line with the their resource growth and the uranium price.

As you can also see SMS appears to be significantly undervalued compared to its peers not only in Namibia but also against all other ASX listed uranium companies –with small JORC resources. For example see:

Koba Res (KOB) with a 4.5mlbs Jorc has a market cap of A$15 million , Marmota Res (MEU) with a 5.4 mLbs Jorc has a market cap of A$38 million, and even compared to some ASX-listed greenfield uranium explorers with soil samples and drill hits but no measured resource For example see:

WCN- A$30 million

DEV -A$55 million

I88 – A$19 million

ORP – A$10 million

Competent Management.

Developing a resource well depends greatly on management. We like that SMS is run by geologists not lawyers and financiers.

The Cobra development will be led by Kiwi Geo Ashley Jones who holds degrees in both geology and finance, and much more importantly, has over 20 years’ hands on experience of successfully developing Uranium projects in Africa and Australia.

-Ashley previously worked for Nova Energy developing the Lake Way Uranium resource WA which was then acquired by ASX listed Tora Energy (TOE).

– He moved to Botswana as general manager of ASX listed ACAP Resources (ACB) developing their Lethlehkane Uranium resource – which grew to become the world’s second largest biggest undeveloped uranium resource. ACB was recently taken over in a stock merger with ASX listed Lotus Resources (A$ 490 million market cap).

Ashley has worked in Namibia previously for some years developing a Manganese resource and held a seat on the Council of the Namibian Chambre of mines. He has been trying to acquire what he believes is the highly prospective Cobra project for several years now, and only recently managed to secure it.

We like the new deal structure as it entails no great up-front dilution for SMS. And if things progress as hoped SMS can earn the lions share, but if things don’t work out they can walk away without too much dilution or loss.

The outlook for Uranium.

Most members are aware of our bullish longer-term outlook for Uranium:

In summary

The world is increasingly turning to nuclear power as it’s the only green power to allow full baseload power.

– New fleets of reactors are coming online all over the world.

– After a multi-year glut and low prices Uranium is again in short supply through underinvestment in mines.

– This short supply looks set to continue until several new mines can come on stream- which can take years, therefore the uranium price is rising again and looks set to climb higher.

– The Uranium price has risen 340% from its low of USD 18 per Lb in 2016 to USD 80 per Lb today. It has hit as high as USD 100 per Lb.

– We believe the uranium price will continue to strengthen over the next years giving upward momentum to most global Uranium stocks.

A Summary of why we like SMS potential:

SMS has most the attributes we look for in our potential 10bagger portfolio pics

1. A cheap, undervalued entry price.

2. A tight share register

3. Competent management invested in the shares and aligned with shareholders.

4 Low downside potential if it goes wrong, plus a sunstantial proven gold asset to protect the shareprice downside.

5. A new prospective asset that the market does not yet fully understand. And one which if successful could allow the share price to rise up more than 10x. – So with little downside if Cobra turns out dud – and a big potential upside if it’s not – we are happy buying and holding SMS at these levels.

Risks: Developing Cobra is a risky business. It will mean further cash raises are required incurring more dilution of the company. Plus it will take time to develop such an asset. SMS will require patience from its investors. The chart below shows the time it took XTR to develop the Husab resource from its first discovery in early 2008 to prove it up to a 480 Mlb’s A$ 2,2 billion Giant by late 2011. But Patient shareholders bought in early and held were very well rewarded.

DYOR (Do Your Own Research) and good luck.

The following website for more detailed information on Erongo’s mines: https://world-nuclear.org/information-library/country-profiles/countries-g-n/namibia

2Portfolios is a members information sharing club with 2 model portfolios:

1. Our 10 Bagger Portfolio concentrates on finding higher risk high return equities (mainly in the ASX) and has so far averaged annual returns of 465% per year for four years.

2. Our Freedom portfolio concentrates on finding International high-yielding equities. And has averaged annual income of 25.3% per year in dividend and growth income over four years.

We also run a discord chat line where members have 24 hour access to chat about latest stocks ideas and market trends.

For more information contact us at: info@2Portfolios.com

or visit our website at https://2portfolios.com

Disclosure: Our club investment committee first entered SMS in our 10 Bagger Portfolio at 3.4 cents in April. 2024. Some of our club members and club principals already hold shares in SMS at the time of publishing this report.