West Coast Silver (stock code WCE.AX) – Target price A$0.40c ++

Our latest 10-bagger call is WCE a silver mine developer listed on the ASX

We first called WCE as a potential 10 bagger stock to our members soon after WCE acquired the exceptionally high-grade Elizabeth Hill (EH) Silver Project in Western Australia. We believe WCE should 10-bag (go up by 1000%) because:

- As WCE develops the highly prospective EH project it should cause a big revaluation upward in WCE’s share price.

- We believe we are in the early phase of a new silver Bull market which should aggressively lift all silver shares higher, and particularly shares in promising smaller, primary silver companies based in good jurisdictions – like WCE.

Our initial price target is 40 cents for WCE within 24 months, but much higher if the expected silver bull run happens.

Why we think WCE could rise by 1000% or more.

- Silver is entering a generational bull market which should drive WCE much higher over the next 24 months.

- WCE holds an under-explored, exceptionally high- grade silver resource open on all sides with the potential for substantial resource expansion in its prospective 180km surrounding tenement.

- Re-opening production at the EH Mine should be quick, require comparatively low Capex and Opex, and be very profitable to operate due to its high grades.

Elizabeth Hill (EH): The Project Background:

First discovered in 1998, EH contains a shallow, near-surface and extremely high-grade silver resource of 46.8Kt at 2,799 g/t Ag, indicating a pre-JORC primary silver resource of around 3.6 mill oz.

EH was open pit mined in 2000 and in its first year of operation, 16,830 tons of ore was mined at an outstanding average grade of

77.4 Oz/t for 1.2 million oz silver making EH Australia’s richest ever silver mine. It also produced 140 kg “Karratha Queen”- the largest pure silver nugget ever found in Australia (see opposite)

In 2000 silver fell below $5 per oz in 2000 and a dispute amongst the partners meant the EH mine closed after year of operation.

Now, with the silver price 700% higher, (AS 58 per oz), WCE have acquired the mining rights over EH and have consolidated a highly prospective 180sq Km tenement around EH. They are now undertaking further exploration to expand the resource and plan to restart production on this extremely rich resource ASAP.

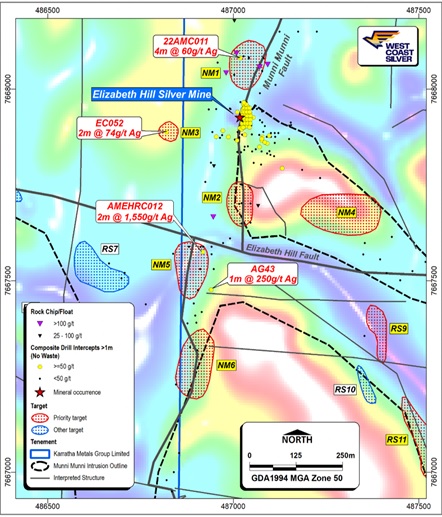

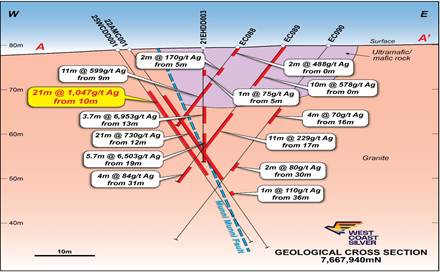

The EH silver resource is near-surface and open on all sides. WCE have just completed 12 drill holes around the EH lode. 4 of these drill assays have been returned from the labs and all confirm further extremely high-grade silver hits. We feel the remaining 8 drill hole assays expected over the next few weeks could provide further highly positive news flow for WCE. (See the attached WCE decks for more detailed drill information).

WCE recently completed a A$6 million cash raise to fund further exploration drilling and re-start production at EH.

The EH Resource Has Significant Growth Potential:

The area around the primary EH silver resource is lightly explored. We believe further drilling could significantly extend the resource.

WCE have targeted 20 prospective surrounding sites for drill testing try to locate additional outlying silver lodes, as their geological consultants believe it’s unlikely a resource as rich as EH is a stand- alone feature. (see map opposite).

The EH silver resource lode sits on the highly prospective Munni- Munni fault line which dissects WCE’s tenement from north to south for over 25Kms. Rock chip and soil samples taken up to a kilometer from the EH resource indicate an elevated presence of both silver and gold. The Munni-Munni fault is also known to be highly prospective for gold, copper, nickel and other base metals.

Fast Track Potential to Production:

- Some of EH mine infrastructure, including roads and 2 head frames from the previous owners are in still place from the previous owners.

- WCE already holds a granted mining license and most other permits to allow them to fast-track EH back into production.

-An unused suitable processing plant sits 25 kms away and is available to WCE which could greatly reduce their CAPEX.

- The high-grade, shallow, EH resource, should require low strip ratio’s and lower OPEX to open-pit mine (The average primary silver mine today operates profitably at grades of around 150 g/t Ag. The EH resource is indicated to be over 10-15x higher grade) and as the saying goes “Good grades make a good mine”.

Potential Costs, Revenues, and Profits:

At this early stage we can only use EH’s previous production to get some indication of the potential future revenue and profitability of the EH mine and therefore some indication of the potential for the WCE share price (SP).

Disclaimer: The projected calculations we use below are speculative, forward looking, and non-JORC compliant. They are calculated independently by 2Portfolio club analysts, not by WCE. They should be considered only as a rough indication for our private club members only, to try to show our own independent indication of the potential for WCE’s future share price.

Share price Forecast Based on Potential Revenue.

If EH produces the same as reported in 2000: 1.2 million Oz Ag from 16,800 tons of ore (77.4 Oz p/t), at today’s silver price (A$58 per oz) it would represent potential revenues of around A$70 million Pa.

As Junior ASX producers usually trade around 1-2x revenue, this indicates a potential future market cap for WCE of between A$70- 140 million. As WCE currently has 320 million shares on issue, that could represent a potential SP of 20-40 cents?

However, mining only 16.8K TPA is a tiny operation, (only about 5-6 truckloads of soil per day). If WCE could operate at a less modest volume of say 50K TPA at 77.4 oz PT, that could increase potential annual revenue to around A$224 million and therefore could indicate a potential SP of 70c -$1.40?

Share price Forecast Based on Potential Profitability. We estimate that a high-grade, open pit mine like EH should not have AISC of more than A$25 per oz to produce? Therefore, using EH previous reported low production of just 16.6K TPA for 1.2 mill oz, at todays silver price of A$58 per oz, infers a potential pre-tax profit of around A$40 million p.a. Depending on the eventual EH

resource size and projected mine life, WCE’s SP could be priced at a PER of 3 to 5 x, If so, that would indicate a potential future market cap of between A$130 – 340 million, or a potential SP of 40c-70c.

Two Caveats to our above Predictions:

- By production time, WCE could have more shares on issue which would dilute our potential projected per Share price assumptions.

- Conversely, an increase in the resource size, the mine production rate, or the silver price, as we expect, would significantly increase our potential projected SP assumptions for WCE

Additional Upside Potential from other Metals:

The Munni-Munni fault which dissects WCE’s EH tenement shows elevated indications of other and metals , plus WCE owns four other prospective tenements in WA, (See tenement map below) These include:

The Errabiddy Tenement: where Falcon Metals (FCM), working on a farm-in JV basis, recently identified a potential 5.2Km long strike sampling up to 1g/t gold from surface samples. Errabiddy sits beside BNZ’s 16.4 million oz Glenburgh Gold deposit.

The Andover West Tenement: adjoins the former AZS tenement where sufficient Lithium and nickel was discovered that AZS was bought-out last year for A$ 1.7 billion.

Work on WCE’s other prospective tenements is currently being funded through farm in JV’s and paid for by other companies. WCE’s prime focus now is only developing the EH silver project. Any further developments on WCE’s other tenements will just be icing on the cake for shareholders.

The biggest potential upside for WCE is the silver bull market we believe is just starting.

The 2portfolios.com investment committee believe we are in the early stages of a generational new silver bull market. Silver bull markets drive most of the worlds 80 or so listed silver companies irrationally high. Particularly those of smaller cap companies in good jurisdictions with primary silver projects and high-grade resources – like WCE.

Indicators that a Silver Bull Market is Imminent:

The on-going and growing global Silver Shortage. Depending on which figures one uses, last year the world produced just under 1 billion oz of silver- but consumed over 1.2 billion oz. (a 20% annual supply deficit).

There has now been a growing silver supply deficit each year since 2020. So far above ground warehouse stores have filled the gap but those inventories are now almost gone.

In 2024 COMEX declared that global above ground stores of deliverable silver for futures settlements, which normally sit around 200K oz had fallen to under 30K oz and this year they may be fully depleted. Paper trading on the futures markets is over 100x times the volume of physical silver mined each year. If there are no silver stores left for physical delivery, we should then see a silver short squeeze that could drive up the silver price by up to 1000%, just as happened in the last two silver bull markets in 1980 and 2012

The worlds Silver Supply is Insufficient and Inelastic. 80% of global silver is mined only as a by-product from mines for other metals like copper, gold, lead, and zinc etc. So even if silver prices rise drastically, supply is limited to demand for the other primary metals and can’t respond efficiently to a silver price rise.

Primary silver mines and recycling only produce 20% of world supply and many of the bigger global silver mines are depleting, or suffering from years of “high-grading” and simply can’t increase production levels to keep up with with the fast-growing industrial demand for silver from the new green and electrifying world.

There have been almost no “big” new silver resources discovered for well over a decade, and even if there are it takes many years to develop them and to extend old mines to significantly increase production.

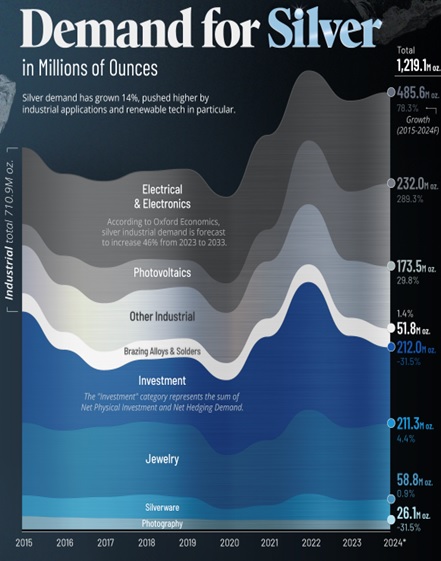

Global Demand is Growing Fast, Outstripping Supply.

Silver is the most electrically conductive metal in the world. Therefore, the huge expansion in global electrification is causing a huge increase in demand for silver in various new industries.

In 2024 80% of world silver supply went to industry.(see chart above) for traditional use in jewelry, medical instruments, silverware and religious Icons, plus the fast-burgeoning demand from the new “green” economy sectors of EV, AI, and mainly solar .

Solar demand for silver is underestimated.

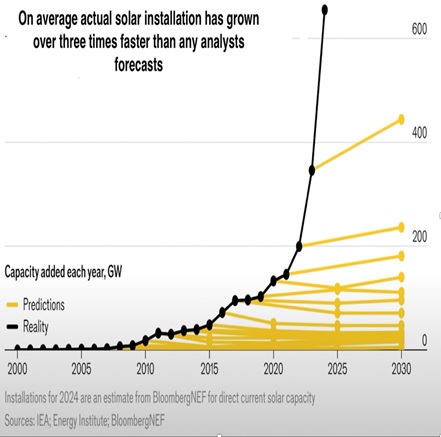

In 2023 solar became the worlds’ cheapest form of power generation. Now global solar installation is growing exponentially and has always significantly outperformed all analysts’ forecasts by a factor of 3-4x.

We believe analysts continue to grossly underestimate the fast rate of global solarization, especially with the recent explosion in PPA financing facilities meaning it is now virtually free to install solar power up front.

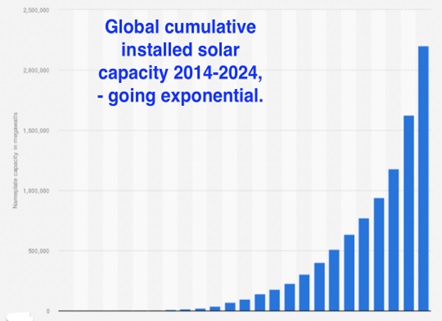

In 2020 under 5% of the worlds silver production was used in solar. In 2024 over 20% was. Installed solar capacity is now forecast to double in under two years. But we feel this is likely another under- estimate by analysts – solar installation globally is now growing exponentially (see below : Source Statista)

Just Do the Math’s:

Taking an average of the Industry figures produced:

- In 2024 the world produced 1 bill oz of silver and used 1.2 bill oz.

- 220 mill oz were used for investment purposes (Bars, coins etc.)

- Almost 1 bill oz were used in industry. Of that:

- 250 mill oz were used in solar.

- 750 mill oz were used by in the rest of industry. (non-solar)

Demand from the rest of industry is forecast to grow at around 8% per year- driven mainly by growth in the EV, AI and electronics sectors. Therefore, this year the “rest of industry” should use around 810 mill oz. and around 860 million oz in 2026.

0.6 oz silver per solar panel

Despite ongoing attempts at “thrifting” (reducing silver input) each solar panel still uses around 0.6 oz an oz of silver. It is estimated over 7 billion panels have been installed globally. Last year almost 500 million solar panels were installed requiring the said 250 mill oz of silver. This year almost 700 million more panels are estimated to be installed requiring almost 420 million more oz of silver.

In 2026 – it is forecast that almost 1 billion panels will be made requiring around 600 million oz of silver. And with the rest of industry forecast to need 860 mill oz, this implies that next year

1.45 billion oz should be needed just in industry alone.

The worlds mines and recycling plants are struggling to produce much over 1 billion oz now, so the supply deficit by next year could reach a huge 40% – just for real industrial needs alone– and that would leave zero silver available for new investment capital.

Investment demand – the elasticity of greed.

Investment demand for silver is the most elastic part of silver demand and can explode up immediately. And one thing that we all know attracts investment capital fast is a rising price.

So as the silver shortage for industry should push price higher, even more investment money will rush into silver: Into Physical silver, paper silver, ETFs, and silver miners and mine developers shares,

Extreme cyclicality happens frequently in most smaller commodity markets. It starts as both producers and traders sense shortage and start holding back inventory to get better prices later. This exacerbates the shortage and the price surges even faster.

The stocks in such commodities producers also get driven very high often to irrationally high levels, (see the antimony or titanium companies now, or more recently the huge gains experienced in Uranium, Lithium, cobalt and REE stocks.)

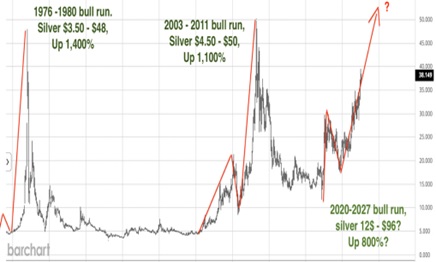

The chart above shows that that in the last two big silver rallies the silver price spiked up over 1000%. And that was from investment demand only and without fundamental shortages from industry – this next bull run could be just as or more intense.

As silver stocks are even more “leveraged” against the silver price – as the marginal profit portion from sales grows faster that the overall silver price rise. So silver companies share prices usually rise by more than the silver price – as has happened in all the last silver bull markets where share price rises of 10-30x were common.

If we take US$17 (in August 2022) as the start of this current developing silver bull market, and if history repeats itself, this bull run could mean the silver price reaching as high as US$170 (A$250). At that silver price just imagine how high WCE the share might reach in such a bullish environment?

Technical Indicators of a coming silver rally:

The gold price as lead Indicator. Gold always rallies first and then silver follows some months later and usually moves up higher and faster. The gold price started to rally a few months ago and so we feel silver should leap higher soon, as it usually does.

The silver gold ratio

Silver is 15 times more common on the earth than gold. For centuries it traded at one 15th the gold price. Over the last 50 years however the average gold to silver ratio has been 57x. Gold is now up to 91x the price of silver and the higher the ratio the more chance there is if silver will rally to catch up with gold.

A Giant Cup and Handle

A cup and handle pattern is one of the most bullish technical indicators. Silver price chart below looks like silver is forming giant 50-year cup and handle. If the price breaks the US$ 50 neckline it indicates the silver price should then move aggressively higher.

Is the Coming Silver Bull Market Guaranteed?

No, of course not, but as Billionaire Jeff Bezos has stated:

“If you see a 10% chance to make 100x return take it every time”. The 2portfolios club investment committee shares his sentiments. In just the five years since our inception we have picked 19 stocks or investments that have risen over 1000%)

To make that strong track record. We need to pick stocks with big potential upside but limited downside if things don’t pan out as hoped. Above we have laid out why we are bullish on WCE, now let’s consider the potential downside.

The Risks and Downside potential

1 The Drill results don’t pan out so well. While this would stunt upside momentum EH already has a known, high-grade resource which we believe can underpin the share price at around 20-25c.

- Management errors: WCE has an experienced management team with a solid track record, who own shares in WCE and are aligned with shareholders and should avoid excessive dilution.

- Financing risk: WCE has A$6 million cash on hand and broker support to be able to raise further money if required.

- The silver price falls: Given that the global supply deficit has been going for 5 years and industrial demand keeps rising. Which has pushed the silver price up 70% over the last two years – and still the chronic supply deficit grows. We feel It is unlikely we should see any silver price collapse in the next 24 months.

- WCE is cheap relative to its global peers: At just US$ 37 million market cap WCE is still cheaply priced compared to most its global silver peers with similarly promising assets.

- WCE is priced at 28% of its IG value: The EH Resource is already indicated at 3.2 million oz, at A$58 per oz this gives WCE an IGV (In- Ground Value) of A$208 million. The current market cap of WCE is A$58 million. So WCE is trading at 28% of its current IGV asset which is a reasonable valuation.

6.USD debasement: As the US$ continues to be debased from the inevitable overprinting of new fiat money, it is most likely both gold and silver will continue to rise in price in dollar terms, which should also support the market value of WCE longer term.

WCE Research Report August 2025

WCE is a stock with low downside, and a huge potential upside over the next 24-36 months. It is the sort of investment we like to hold in our aggressive 10-Bagger portfolio.

NOTE: The 2Portfolios club first informed members that we were adding WCE into our 10-bagger Portfolio at 3.9 cents per share in April soon after WCE acquired the Elizabeth Hill Silver Project.

Our club policy on smaller or less liquid companies is to wait a month or so before informing associate members and releasing research publicly about our new ten bagger calls to give our paying club members sufficient time to accumulate share first. Membership USD 100 per year.

WCE’s share price has already moved up a fair bit, but as WCE further explores and develops the EH project, and as the silver price should continue to move higher due to increasing global shortage, we believe WCE has much further to appreciate.

Disclaimer: This research report is made for members and associate members of 2Portfolios private investment information sharing club. It is written by experienced club analysts. The information contained is based on information provided by WCE to the public market and general silver market information sources and is designed to give members an indication of what our club investment committee think could happen to WCE shares in the future. The information contained is speculative, forward-looking, and non-JORC compliant, and there is no guarantee that any of our assumptions may prove correct, it is only our suggestion of what we feel could occur to the WCE stock price based on our investment committees long combined investment experience.

This is not investment advice. Investing in exploration or developing mining companies can be very risky on many levels and could result in you losing a lot of, or even all the money you invest. Therefore we strongly suggest all members do their own research before investing, and for investment advice you should discuss with a qualified investment professional about the investment risks and whether WCE may be a suitable investment for your portfolio.