A new 10 Bagger call: HVY.ax

We recently called ASX listed Garnet mine developer Heavy Mineral Ltd: (ASX stock code: HVY) as a new potential ten-bagger stock. The price today is 12 cents. We believe, that without any black swan events, HVY’s share price could reach more than A$1.20 within 24 months.

New Royalty Funding

Yesterday garnet mine developer HVY, announced that it has received A$2.1 million in royalty funding, (a loan against a 1% of future mine production income). Royalty funding is a non-dilutive way of funding resource developments.

This is good news for HVY shareholders as it means HVY now has the funding to complete its Pre-Feasibility Study by year end without diluting shareholders excessively by selling undervalued shares as per normal cash raises on the ASX.

So hats off to HVY for pulling this royalty funding off. The funder is Campbell Transport, HVY’s designated transportation company for when the mining starts. It’s good to see such belief and co-operation between partners.

HVY is very Cheap

HVY currently has only 63 million shares on issue, at 12 cents a share this gives HVY a market cap of just A$7.5 million.

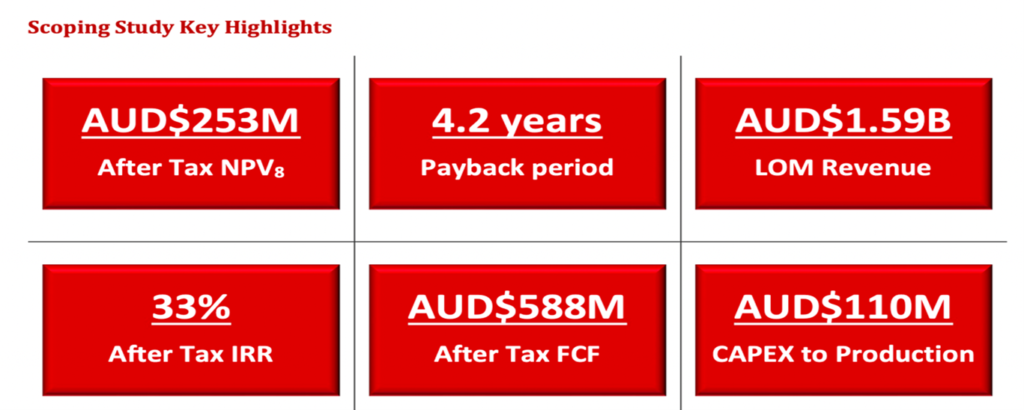

This is very cheap as their independent scoping study in 2022 on their Port Gregory Resource gave HVY a NPV (Nett Present Value) of A$253 million. Since then, HVY has increased its JORC resource by around 30%, which we estimate should increase its NPV now to well over A$300 million. This valuation also ignores HVY’s highly prospective Red Hill Resource to its south.

HVY’s Projects

HVY is developing two Almandine Garnet resources In West Australia (W.A) : Port Gregory and Red Hill (See map below). – These also contain Ilmenite and Zircon as saleable by-products.

HVY’s Port Gregory resources directly adjoins the privately owned GMA mine currently – the biggest garnet mine in the world, which has been running profitably for over 50 years. (but is now suffering depletion issues).

On the other side of the GMA garnet mine is the Lucky Bay garnet mine being developed by ASX-listed RDG, which currently has a market cap of A$85 million (10x more than HVY).

What is Almandine Garnet used for?

Garnets are the red volcanic stones used in jewellery– but garnet (without the s) is the shards of garnet found in ancient beach sands.

Garnet is used mainly as an abrasive in waterjet and sandblasting, to cut steel and strip paint and rust in the maintenance of shipping, military equipment, oil and gas installations, bridges and other infrastructure and metal surfaces exposed to the elements and corrosion. It is also used in filtration.

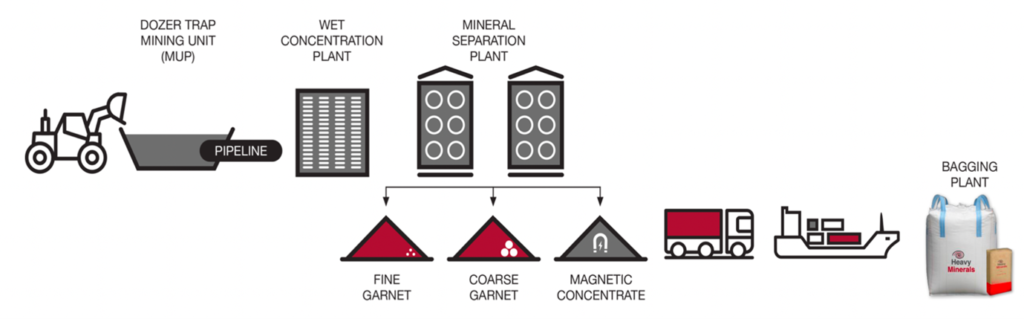

The garnet mining process from sand is exceptionally simple. Just dig the sand and separate the garnet in a simple plant, bag it, and ship it – this simple process entails both lower Capex and lower Opex.

Mining Garnet from Sand is Simple…

The Global Garnet Market

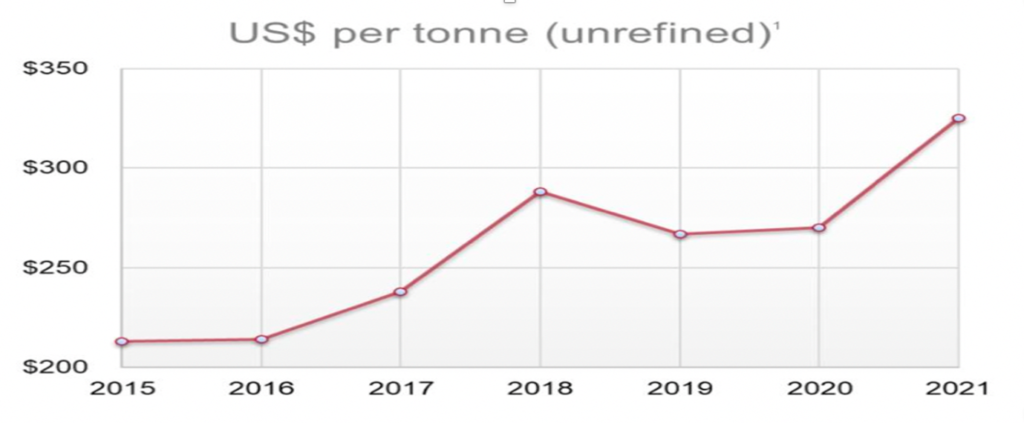

Almandine Garnet sells for around USD 550 (A$800 per ton) depending on the garnet characteristics, – from their JORC work to date, HVY seems to have premium type Garnet.

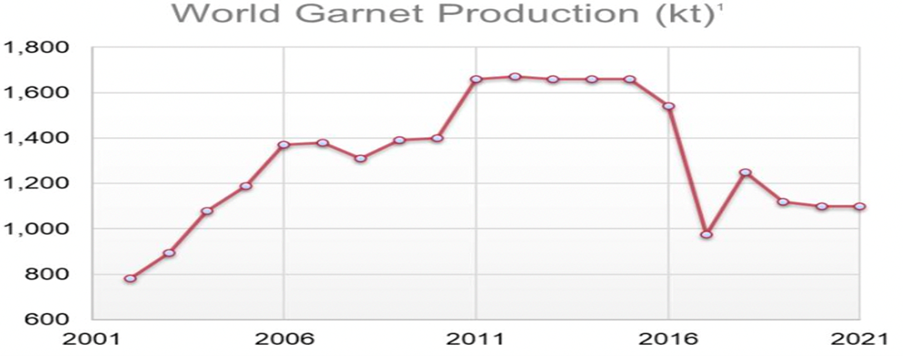

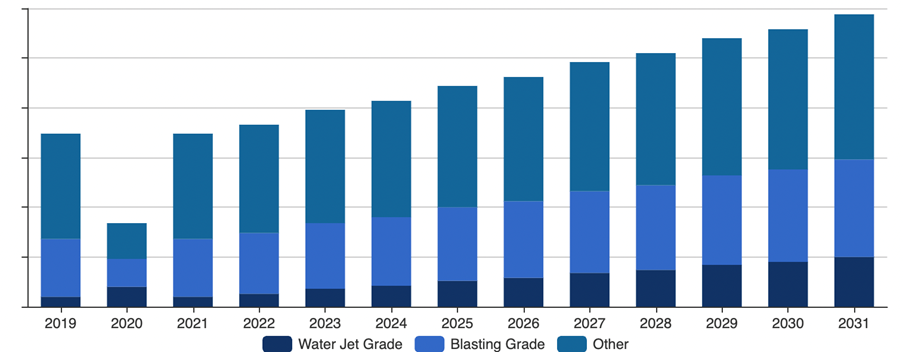

The Garnet market today is about 1.8 billion tons annually and growing, which sells for around USD 1 billion (A$1.5 billion) per year.

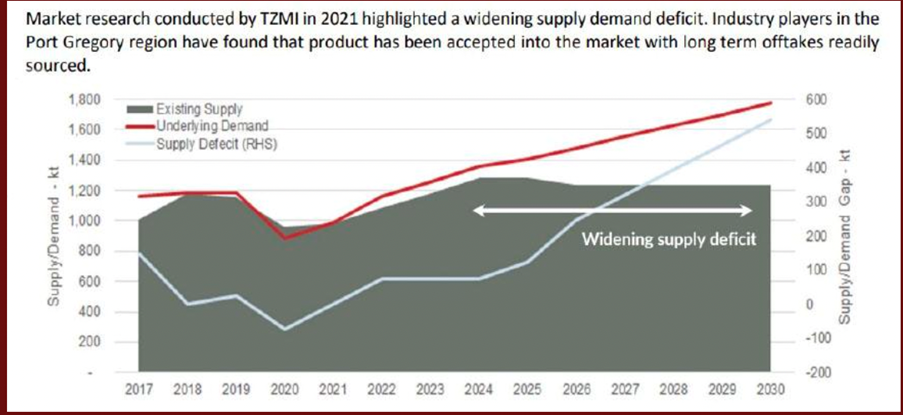

The main global suppliers have traditionally been India and W.A – however, India recently banned sand mining for environmental reasons, this has massively reduced their garnet production, causing an approximate 500,000 ton (30%) short fall in global supply each year which needs to be filled.

With increasing amounts of aging infrastructure globally, rust and corrosion is estimated to cause losses of over USD 3 trillion a year globally – around 3% of global GDP. Therefore, the Almandine Garnet demand globally is anticipated to increase by a CAGR (Compound Annual Growth Rate) of around 6.5% per year over the next 10 years.

Therefore, the garnet price is rising, and garnet buyers today are under pressure to secure new long-term offtake deals from new and reliable sources of supply such as W.A.

The forecast demand deficit for Garnet to 2030.

Garnet demand keeps growing and supply is limited…

….So the garnet price is expected to continue rising

Global almandine market growth by use type 2019 – 2031

Why do we think HVY’s share price could 10x?

HVY’s Port Gregory Scoping study (see above) indicates that for Capex of around A$110 million, HVY can get into production in late 2026 and should expect to make over A$40 million a year in post-tax profit for an estimated 20 year mine life.

A$40 million in profit, divided by what we expect should be around 75 million shares when HVY goes into production, imply a potential profit of around 50 cents per share. If we value that on just a modest 5-6 x PE ration, it implies that – (if all goes as planned in the SS), that HVY’s share price could appreciate to reach around A$2.50-$3.00 per share in around 24 months.

The HVY share price today is 12 cents – which is why we believe this stock has the potential to 10x its current price over the next 2 years or so.

Full 2Portfolio members first got in to HVY from 5 cents.

We first called HVY to our members a month ago at 5 cents a share. But as per our club policy, we waited some time to send out this email to all associate members to give our paying members time to accumulate first.

Early entry into our calls is a benefit of becoming a full member. – For example, in this case, had you invested A$20,000 in HVY at say 6 cents average after our call – that would now be worth A$40,000. – your A$20,000 profit would cover our modest USD100 annual membership fee for about 200 years!

Can you really afford not to join?

2Portfolios have now called 14 ten bagger stocks in 4 years, you only need 3 to become financially free.

But don’t fret, even at 12 cents, we think that HVY still has the potential to 10 bag (rise by 10x) – or at least move significantly higher, over the next 24 months.

How will HVY get the Capex to get into production?

The current funding for HVY means it can now complete its Pre-Feasibility Study. Once that is done it should become easier for HVY to acquire further royalty loan funding from the increasing number of global royalty funds available. Last year in the USA almost 50% of resource development funding came via royalty funding.

HVY has already announced signing a financing proposal with Atradius, a Dutch government export finance fund to loan finance the plant.

Due to the current under-supply of garnet, we feel that HVY should also have the opportunity later to sign pre-paid offtake agreements for early funding – HVY has signed one offtake MOU already, two years before production.

There is also W.A development grants, potential bank-financing and or of course cash raising from share sales, – which becomes more plausible as the HVY share price re-values higher as expected.

What are the risks?

Getting funded: In all resource development there are always development and delay risks. We see HVY’s main risk is that as a small-cap company it may have issues and delays to obtain the full Capex funding required to go into production as anticipated above.

The Garnet market is small: at just around A$1.5 billion a year in value, the Garnet price could be volatile in the future and could be adversely impacted by reduced demand or new sources of supply.

DYOR (Do your Own Research)

As always, we suggest members should DYOR, and take advice from a professional advisor if you have any qualms about buying HVY. If you do decide to buy, then buy cautiously and slowly. HVY shares are relatively illiquid and can be volatile or could run higher if you buy too aggressively.

Disclaimer: This is not advice to buy. We are only sharing information and research – which is what our club does. The above forward-looking figures are speculative projections from our analysts based on HVY’s independent Scoping Study. They are not official figures from HVY.