A FINANCIAL INFORMATION SHARING CLUB FOR MEMBERS : 2PORTFOLIOS.COM. 02/10/24

Heavy Minerals Ltd. Stock code HVY.ax

An updated report on our current top 10 bagger pick, Australian Garnet mine developer Heavy Minerals Ltd, HVY.ax. We first called HVY at 5 cents in July – the price at time of writing 8.8 cents.

HVY stats.- on date: OCT 2 2024

Shares on issue : 67 million shares on issue Current share price: A$0.088 cents

Market cap: A$5.9 million. (USD 4 million).

Cash available: A$ 2.1 million. (current exchange rate is A$ 1 = US$ 0.69)

We believe HVY is extremely undervalued against any valuation of its assets, potential and competitors: See examples below: HVY is currently valued at just A$5.9 million or A$0.088 cents per share.

- HVY has a proven JORC resource of Garnet (plus Ilmenite and zircon as sellable by product) giving it, at today’s Garnet prices, an In-Ground Value (IGV) of around A$ 4.9 billion. In North America a normal rule-of-thumb valuation for any company with a proven JORC resource in a good jurisdiction (like Australia) is around 5-10 % of its IGV.

Under this measure HVY should be valued at between A$245 -490 million. With 67 million shares on issue that implies HVY share price should be around: A$7.30- $3.65 per share

- In 2022 IHC Mining – a large international mining consultancy and valuer accepted by all stock Exchanges – completed an independent Scoping Study (SS) and give HVY an NPV (Net Present Value) today of A$311 million. Divided by 67 million shares that’s: A$4.64 per share.

- In their SS IHC forecast HVY could start mine production in late 2026 and make over A$40 million post-tax profit annually with a mine life of 21 years. Divided by 67 million shares that would be A$0.59 cents per share profit per year. If we put that on a modest 8 x PE ratio, HVY shares could reach around A$4.70 per share

(Even if we imagine a 20% dilution for future cash raisings (see below) a significant price rally in HVY shares looks immanent).

- RDG.ax, another ASX listed company is starting a similar sized Garnet mine 4kms north of HVY. RDG is about 20 months ahead of HVY in getting to production. RDG has market cap today of A$74 million. At a similar valuation would price HVY shares around: A$110 per share

The Global Garnet Market.

Garnets (with an s) are the red gems from diamondiferous volcanic pipes used in jewelry. But Garnet, (with no s) is the broken garnet shards eroded over and washed away and found clustered in a few rich catchment areas in the world – open ancient beach sands like on the coast of West Australia around Port Gregory. Like industrial diamonds, garnet is very hard and sharp so garnet shards have recently become the abrasive of choice in global water-jet blasting for paint and rust stripping and for cutting metal.

Corrosion and rust is a huge problem globally – costing economies around USD 2.5 trillion annually -or 3.5% of global GDP. Infrastructure, Ships, bridges, oil and gas installations, heavy outdoor equipment, buildings and military vehicles all need to be regularly sand blasted and repainted and industrial manufacturers need to cut metal – so garnet abrasive sand is in growing demand globally.

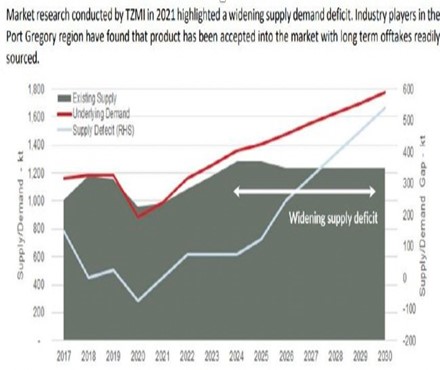

Last year 1.8 million tons of garnet sand was purchased. The Biggest buyers are the US military and Saudi Aramco. Garnet sand costs around A$900 (US$ 600) a ton today, valuing the global garnet at around A$1.4 billion last year. But the garnet price is moving higher due to supply shortages.

1 Short-term: About 70% of world Garnet supply historically came from West Australia (WA), China and India. But India recently banned sand mining due to ecological damage which has cut world garnet supply by 25% (300,000 tons annually) creating an acute shortage.

2.Long term – as more infrastructure ages in richer economies and as the many economic benefits of garnet sand as an abrasive over its competitors are realized, more and more garnet is needed – but traditional mines are depleting and finding new resources is hard and developing them into substantial producing mines take years. So, the shortage looks like it will continue for a long time.

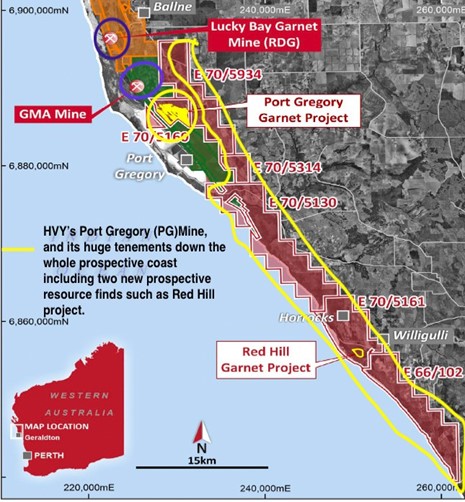

The coast of W.A by Port Gregory (PG) holds the world’s richest known concentrations of garnet.

HVY now owns most mining rights in the PG area. (see map above) –

Directly Abutting HVY’s PG project is the GMA mine, -the biggest Garnet mine in the world. It produced 30% (350,000 tons) of the world garnet supply last year. – Just 4km further north is the Lucky Bay Mine, with a similar sized resource and mining volume plan to HVY.’s PG project – HVY has also just located two new large prospective garnet resources on its tenements- The one at Red Hill to the south looks potentially huge (maybe bigger than PG) and further exploration and drilling to define it continues.

Background to HVY.

In 2021 HVY had acquired most the garnet-prospective tenements on the Port Gregory coast then IPO’ed on the ASX and raised A$5.5 million, at 20 cents per share, to develop them. Over the last 3 years HVY spent that money identifying and developing their PG garnet project to JORC standard. In 2022 they hired IHA mining (a global subsidiary of Dutch Royal IHC) to do an independent Scoping Study on their PG project. IHA forecast that HVY should be in production within by 2026 for around A$75 million Capex (recently adjusted down) and thereafter forecast HVY should make A$40 million post tax profit per year. HVY have now hired IHA to complete a full PFS (Pre-feasibility Study) prior to starting to construct their mine. This PFS is expected to be completed by Jan 25.

Why is HVY share price so low now?

- Most people do not know of, understand or care about the unsexy Garnet market or HVY. This is good at this stage-as they will only likely care and find it sexy when it starts making big money.

- The last 2 years have been rough for all ASX juniors and cash raising has been hard.

- By mid 2023 HVY had used most their IPO funds and clearly needed to do a Cash Raise (CR) – so investors stopped buying shares on market to wait for the cheaper CR shares. Indeed, HVY’s own house broker even sold down the share aggressively hoping to be able to buy new CR shares cheaper.

Adam Schofield, HVY chairman, took the bold decision to not dilute shareholders by selling way undervalued new shares and instead to raise the required capital through early royalty funding (against future mine production). In America royalty funding for resource companies is common but in Australia it has not been used. So HVY struggled to get funded and its share price fell lower. Then last month HVY pulled a rabbit out the hat by raising A$2.1 million via the first syndicated early Royalty funding done on the ASX. HVY is now funded to complete it’s PFS and this should allow the rest of the funding needed to fall into place. (see below) The share price is now starting to recover.

HVY need A$60 million Capex and around A$15 million Opex to start mining. How will they get it?

HVY already have two large European manufacturers competing to sell them the A$60 million-ish plant and all are offering financing options to install it for free and get repaid from future production.

As for the A$15 mill Opex, there are 3 options:

- Once the PFS is completed it opens the door to the billions of dollars in global royalty funds today looking to pre-fund viable new mines in safe jurisdictions like Australia (royalty funds normally don’t invest until PFS is completed). HVY is already in such discussions

- In a market in short supply like garnet today, buyers are willing to pay upfront to secure long term supply from reliable new jurisdictions. HVY have already signed up one offtake MOU and are negotiating with others now on such terms

- As the PG project advances, HVY share price will likely move much higher towards my forecast levels. If need be, at higher prices, HVY could also do a CR without having to issue so many new shares and cause much dilution to existing shareholders

Management

Adam Schofield, chairman, is an engineer and director of other ASX mining companies who specializes in financial structuring. As a shareholder, he wants to avoid unnecessary dilution for shareholders. Aaron Williams -for the last 10 years was the COO (Chief Operating officer) of GMA. GMA operate the world’s biggest garnet mine next door to HVY and GMA sell around 40% of the global garnet supply each year. Aaron set up and ran GMAs global distribution network and personally knows all the major global Garnet buyers. Aaron leg GMA recently as he is aware GMA Mine Is depleting ager 50 years operations – and he believes HVY should become the next major global supplier.

Greg Jones – is one of Australia’s leading sand geologists.

Other reasons to be bullish.

Our valuations above are only based on HVY’s PG project. But once PG starts producing cashflow HVY can then:

- Upgrade its plant to increase production. For example, the GMA mine started with just 3,000 tons a year in 1973 and today GMA produces over 600,000 tons a year from GMA and other mines.

- HVY have located other prospective garnet resources on their WA tenements which look like they could potentially be much bigger than PG.

- HVY also owns a huge prospective heavy mineral and Garnet resource in Mozambique to be developed or sold.

Summary : Low downside -huge upside

AT USD 3.8 million, HVY’s is currently valued at little more than a listed shell company. But owns a huge resource which IMO, at a very minimum, could be sold off for cash of more than 5 times HVY’s current market cap. This means the downside risk on HVY here is low, but the upside is potentially huge, – a 10-50 bagger. To us that’s a good bet.

Disclaimer. The above calculations, research and views are all our own

For more information go to: 2portfolios.com Or contact us at : info@2portfolios.com