IND.AX: A New Potential Ten-Bagger Opportunity

Industrial Minerals Ltd – stock code IND.AX announced today Monday 29th June that it is doing a new Cash raise (CR) which closes today, Tuesday the 30th June at 5pm (Perth).

2 Portfolio members and associates are being offered the opportunity to participate in this CR as we have been long-term supporters of IND.

We believe this CR is an attractive opportunity to enter IND as we believe IND’s share price could move considerably higher over the coming months.

IND is one of our top potential ten-bagger picks on the ASX. (A ten-bagger is a stock that can potentially go up by 10 times)

ABOUT THIS CR.

This CR is being done at 20 cents a share (a 26% discount from last Friday’s close) of 27 cents per share. Plus, you get a free one-for-two attaching option to buy an IND share for 30 cents within the next 3 years. The term sheet is attached to this email below.

If you want to apply for some of this CR please contact Jeff Sweet, the managing director of IND, at jeff@industmin.com.

Disclaimer: The 2 Portfolios Club is not taking any commission or payment for introducing you to this cash raise. It is being done as a free service for all members and associates.

ABOUT IND

IND currently has 68.7 million issued shares on issue. So, at 20 cents per share, this CR values IND at approximately A$ 13.7 million. After the CR IND will have around A$2,200,000 cash and around 87 million shares on issue.

IND is developing High Purity Silica Sands (HPSS) and High Purity Quartz (HPQ)resources in West Australia to export.

IND’s HPSS (sand) business is currently on hold. They are awaiting a better HPSS price so mining it and selling it can become more profitable. We believe this business will add value later. So, we shall ignore the HPSS side of their business in this report.

We believe IND’s HPQ business is what could cause IND’s share price to rise significantly within the next 24 months.

IND’s HPQ POTENTIAL

High Purity Quartz (HPQ) is mainly used in semiconductor and microchip manufacturing. – and currently is in huge demand due to the world’s increasing need for computing power. Therefore due to limited global supply the price of HPQ continues to increase.

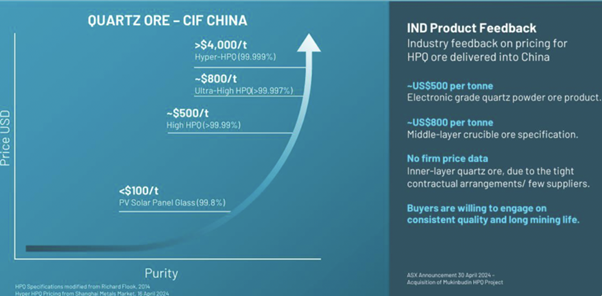

The chart below indicates the current sale value of HPQ depending on its purity levels:

As you can see: HPQ concentrate ranges from USD 100 a ton for 99.8% purity, and up to USD 4000 a ton for 99.999% purity.

Last Friday, (see ASX announcement dated 26 July 24) IND announced that its HPQ had been independently tested in the US and using only basic purification techniques reached levels of 99.991%

Their HPQ is expected, with further advanced chemical purification processes to reach the 99.994%-99.999% range. This means IND should likely be able to sell their HPQ for between USD 700 and USD 3,500 a ton. (see chart above).

Our club’s researchers estimate that IND should be able to mine and ship their HPQ concentrate to China CIF for around USD 250 – USD 500 per ton. This implies IND could make between USD 450 – USD 3,000 gross profit on any offtake agreement from Asian buyers where most microchips are made and HPQ is in strong demand.

IND has stated that it is already in advanced negotiations with multiple off-takers. As their HPQ purity was only independently confirmed last week, IND should, hopefully, be able to sign their first off take agreement within the next months.

IND have announced their resource at Pipingarra is already Jorc proven to 1-3 million tons, where they already have a mine licence and are shovel ready to go.Historic drilling indicates they could have a similar-sized resource at Mukinbudin.

POTENTIAL PROFITABILITY OF HPQ

Note: the following numbers are forward-looking and speculative. They are our club researchers’ best estimates, not official figures from IND.

If we imagine all goes as expected and IND obtain one or two multi-year offtake agreements for, conservatively, around 100,000 tons a year – and IND could make and average of around US$ 600 million gross profit per ton (A$880) that would amount to around A$ 88 million gross profit per year. – Let’s call that approximately A$ 60 million net profit?

A$60 million PA profit on a multi-year offtake agreement – with a potential 20-40 year L.O.M, IND should be priced at least on a 5x PE which could give IND a Market cap of around A$ 300 million.

With an estimated 90 million shares on issue by then, – that would indicate a potential share price of around A$3.30 per share for IND.

The stock market is a forward pricing mechanism. Therefore, we believe we could soon start to see IND’s price appreciate further in anticipation of their first offtake agreement.

If you do want to participate in this IND CR- please get in touch with Jeff Sweet at the email above, preferably before 2 pm Tuesday 29th July, and please use the code 2P to identify yourself as a 2Portfolios club member – as this should help to ensure you may get your fill.

Disclaimer: This is not advice to buy. We are only sharing information and research – which is what our club does. The figures we use here are speculative and there is no guarantee they shall happen. So please do your own research – or take advice from a professional financial advisor before investing.

Good luck, The term sheet can be found HERE. Or feel free to contact us at info@2Portfolios.com

Or visit our website at 2Portfolios.com for more information about our club